Understanding Consumer Credit Graduation Journeys A Key for South Africa’s Economic Growth

- More than one fifth of South Africans graduated to a more complex credit wallet over a four-year period.

- Women hold 55% of credit products in South Africa and are more likely than men to retain a retail credit product throughout their credit journey.

- Personal loans and vehicle finance are most popular first forays into a more complex credit wallet.

- Opportunities exist for lenders to educate consumers so that they can build and maintain strong credit scores along their credit graduation journey.

Lenders that understand consumer credit journeys can more confidently grow according to the findings of a new TransUnion South Africa study released today. The research, presented at its annual Financial Services summit in Johannesburg, examined South African consumers’ credit journeys as they expand their wallets from holding one type of credit product to holding multiple types of credit products that serve diverse needs.

The study analyzed the changes in wallet profiles of South African consumers between December 2018 and December 2022. The study focused on consumers whose credit portfolios were current i.e. non-delinquent at the beginning of the study, because assessing payment history is one of the criteria that lenders examine first when considering a credit application.

The study identified five distinctive wallet profiles among the 7.6 million consumers within its parameters, and excluded the small number of consumers who held retail and secured products, or only secured products.

| Retail Credit Only1 Wallet | Retail and Unsecured Credit2 Wallet | Unsecured Credit Only Wallet | Unsecured and Secured Credit3 Wallet | Full Suite4 Wallet | |

Consumers | 2.1 million | 1.2 million | 1.9 million | 944,000 | 815,000 |

Percentage of study | 27.1% | 16.1% | 25.3% | 12.4% | 10.7% |

Shift in volume over four years | -3.2% | +0.5% | +1.8% | +1.5% | +0.1% |

1 Retail credit include clothing credit, retail revolving credit, retail instalments, or a combination of these

2 Unsecured credit products include personal loans and credit cards

3 Secured credit products include vehicle finance and home loans

4 A full suite wallet includes retail, secured, and unsecured credit products

“Over the four-year observation period window, 13% of consumers in the study graduated to an expanded credit wallet of their own accord. With proactive engagement from lenders, including a focus on credit education, more consumers may be encouraged to graduate from one wallet type to another, more quickly,” said Weihan Sun, director, Financial Services Research and Consulting at TransUnion Africa. “The more that consumers have the opportunity to access and leverage credit products to facilitate upward financial mobility, the greater the level of financial inclusion, and the better the potential for economic growth.”

More than one-fifth of retail-only consumers progressed in their credit journey

Of the consumers who ended 2018 with only retail credit products in their wallets, 21% had added an unsecured product by the end of 2022. At the same time, another 10% had closed their retail credit product(s), but had opened a credit card or personal loan over that time. Three percent of the previously retail-only consumers in the study graduated to a full suite of products, with just 1% closing their retail product but opening secured and unsecured credit lines.

This graduation rate and journey is an important measure to ensure that consumers have the opportunity to use credit to make a meaningful impact to their lives and attain their financial goals. As previously shared in TransUnion’s “Empowering Credit Inclusion: A Deeper Perspective on New-to-Credit Consumers,” 58% of South Africans begin their credit journey with a clothing account. As they graduate in their lifecycle and have greater needs, having access to useful and relevant products for financial inclusion is key to economic growth.

Women lead the way with credit

Of the South Africans in the study, women held 55% of credit products overall. Nearly 70% (69.5%) of consumers in the study that only hold a retail credit product are women, and 54% of South African consumers holding a full wallet suite are women. Retail credit products often cultivate loyalty and repeat spend through targeted special offers or discounts, encouraging consumers to retain them to take advantage of savings and other benefits.

The only segments where men outnumber women were in the unsecured credit-only and unsecured and secured credit segments – neither of which include retail credit. This shows that female borrowers are well represented in segments with retail products, and that they would likely retain their retail products as they progress through their credit journeys. Ensuring that lenders’ offerings and services are relevant to women is a critical implication from this finding.

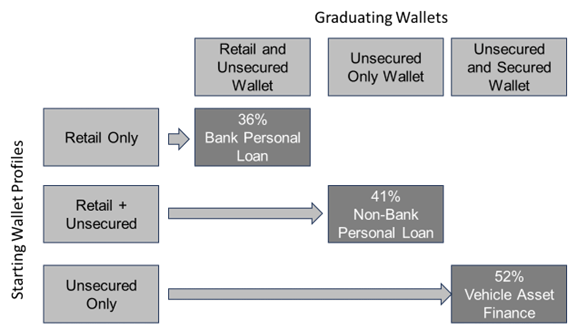

Personal loans and vehicle finance are the gateway to credit graduation

Over the four-year period of the study, 1.1 million consumers diversified their wallets by adding additional credit products. Personal loans were the first choice of 36% of retail-only consumers graduating to a retail and unsecured credit wallet, 29% of these consumers chose non-bank personal loans as they grew into a credit wallet of only unsecured products. Thirty-five percent of those in the study chose vehicle asset finance as the next step in their credit journey to an unsecured and secured credit wallet.

Among consumers who started out (in 2018) with retail and unsecured products in their wallet, 41% chose personal loans to expand their credit wallets, indicating that liquidity is important to support consumption. Of the consumers who started the study period with only unsecured credit in their wallets, 52% chose vehicle finance as their first foray into secured credit, benefiting from access to private transport and the opportunity to build their credit profile even further.

Diagram 1: Consumer credit graduation through different wallet types

“By adopting more proactive go-to-market strategies, particularly in upselling and cross-selling campaigns, lenders could more effectively meet consumers’ changing needs, fostering stronger relationships and promoting sustainable, confident growth,” Sun observed. “TransUnion has identified unique and predictive consumer attributes that lenders can leverage to identify which consumers are likely to graduate and perform better.”

These insights include the observations that performing* credit wallet graduates make fewer inquiries for new credit, and they have longer credit histories on file. They also hold lower non-mortgage and revolving credit balances and display lower utilisation rates on their revolving credit products.

More complex wallets offer better risk prospects

With the study highlighting that bank- and non-bank loans, and vehicle asset finance products are the first choice of consumers as they expand their credit wallets, it is helpful to understand risk distribution across consumers’ wallets as they graduate from simple to more complex wallets.

For example, 23% of consumers who only hold a retail product are prime or above*, with this figure increasing to 50% for the consumer population once an unsecured product is added to the wallet. Of consumers who hold both secured and unsecured credit products in their wallet, 85% are prime or above, with this increasingly slightly to 87% once a consumer has graduated to a full suite of credit products.

Table 1: Risk** Distribution of Non-Delinquent Consumers by Wallet Composition, Compared to the Overall Market

Retail only | Retail and Unsecured | Unsecured only | Unsecured and secured | Full suite | Overall Market | |

Super prime | 6% | 19% | 14% | 56% | 56% | 14% |

Prime plus | 5% | 11% | 4% | 14% | 15% | 5% |

Prime | 12% | 11% | 4% | 14% | 15% | 5% |

Near prime | 12% | 16% | 10% | 8% | 8% | 9% |

Subprime | 65% | 34% | 64% | 7% | 6% | 64% |

“Trended credit scores and consumer attributes measured over time by monitoring the changes in consumers’ credit behaviours can help lenders better understand and serve their customers, by responding to their evolving credit needs,” Sun added. “Consumers who manage their retail and unsecured credit products well, improve their credit profile over time, and hence are able to graduate to take advantage of secured lending products, along with the lifestyle benefits that these expanded wallets offer.

“Lenders should consider a dynamic and tailored approach to cross-selling and up-selling based on each consumer's readiness and ability to manage more complex credit products. By doing so, lenders can drive growth while promoting a healthier, more inclusive credit market that delivers lifetime value for both parties,” Sun concluded.

*A performing consumer keeps their credit repayment obligations current, and are not in default on any credit products

**As measured by TransUnion CreditVisionTM risk scores: Subprime 0-625, near prime 626-655, prime 656–695, prime plus 696-720, super prime 721-999